Bienvenida, welcome, bienvenue, willkommen: volatility

Andorra Expats | 04.30.2018 | David Azcona

Last weekend, for the first time this spring, we were able to enjoy some sun. It was the main topic of conversation right across the country: “finally, what a long winter that was!”

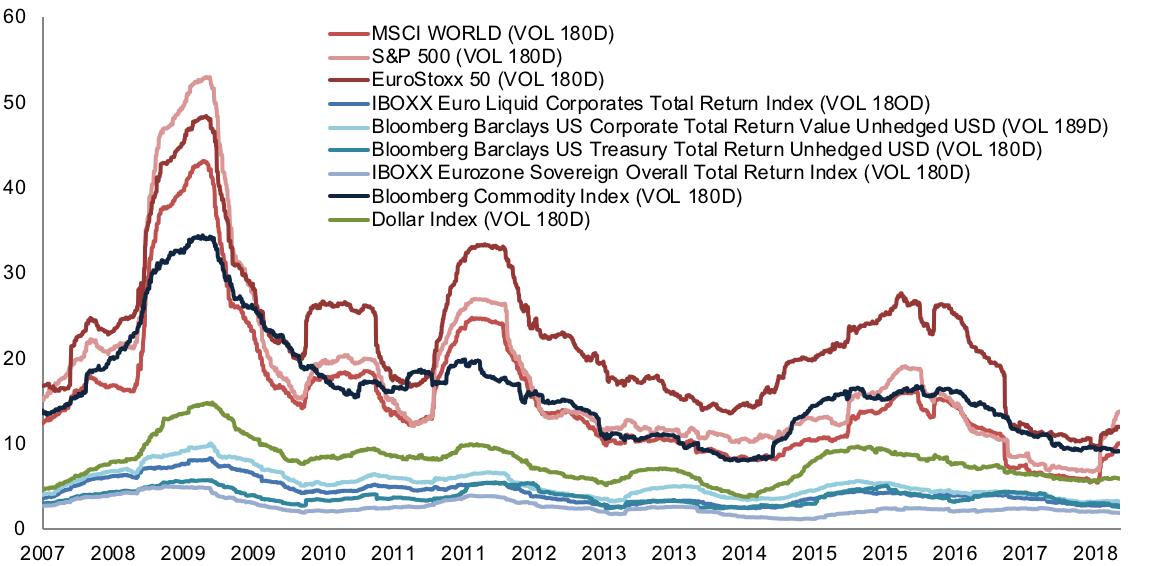

The same has happened to me with volatility (the most widely accepted measurement of market risk). After years during which US markets in particular have shown relative calm and stable returns, the first quarter of 2018 has been accompanied by an increase in implicit risk on several assets, above all equities. Thank goodness! “Why” you be say; because we were witnessing a backdrop of euphoria that ran the risk of triggering serious problems in the future, including in the real economy. A portfolio manager’s work and the proposals they make to clients are based mainly on expected risk and return. Given that risk has been historically low, only those investment houses that understood that such volatility levels were not normal were able to ensure that their clients were correctly advised during the first few months of the year. This warning should serve to ensure that the industry recalibrates its inputs in future, so as to better protect investors’ capital.

Why was volatility so low?

There are structural reasons, such as the new regulation introduced following the last financial crisis, and others such as the growing market share of the new technologies in the investment world. But there are also cyclical drivers, such as the massive asset purchases carried out by most of the world’s central banks. As you will have guessed, I am a firm believer in active management, but the big disappointments suffered by the innovations that kept volatility depressed should make us take stock. I am not suggesting that we go back to the “horse and cart”; but it is not a question of “anything goes” either. We need to be selective, we must stick to the long-term view, maintain well-diversified portfolios, and avoid drastic decisions at delicate moments.

And now what?

What was at first initiated by a mixed bunch of factors (“stranger things” as we called them in our last editorial) has since been spurred on by more trade sanctions and tensions, along with the war in Syria. The result: everyone is searching for the algorithm that best pinpoints the start of the next recession (“One year out, no problem; but two years out is a different story”, as one research house said). Investor sentiment indicators are at their most pessimistic level since February 2016.

In our view, what we are looking at is not the start of a bear market but rather a correction that should not turn into anything worse. It is a good recipe: stable growth levels, leading indicators deteriorating but still close to all-time highs, and a seasoning of earnings that show no sign of changing trend. The feast should continue! Credit conditions remain buoyant and corporate debt has proved extremely solid; and this is the most important thing to watch right now.

Sadly, all sorts of wars have broken out; but fortunately, the different factions are likely to find common ground; there is too much to lose!

Often at investor meetings what we measure is the margin of error, due to the fact that equity valuations and interest rates are way off their historic averages. And what is clear is that there is a window of opportunity opening up that we have not seen for five months.

This article was published on Markets and Strategies, the monthly publication in which our experts at MoraBanc Asset Management analyze and give their vision of the most important international economic news.

Information on the processing of personal data

In compliance with Law 15/2003 of 18 December on protection of personal data, the customer authorizes that the applicant’s personal data entered on this form will be incorporated into files owned and managed by MORA BANC GRUP, SA – MORA BANC, SAU (hereafter referred to as “MoraBanc”) to process the requested service and, if necessary, to comply with the contracts finally entered into, and also to ensure correct operational procedures.

The applicant expressly authorises MoraBanc to send him/her commercial and promotional communications for products and services and information on the Bank itself, social or other activities, in hardcopy by post or by electronic means (among others, short messages (SMS) to mobile phones, e-mail, etc.). This consent can always be withdrawn, without retroactive effect.

The fact of filling out this form implies that the applicant acknowledges that the information and personal data provided are true, accurate and correct; otherwise, MoraBanc declines all responsibility for the lack of truthfulness or correctness of the data.

The applicant authorises the data provided to be communicated or shared with third parties forming part of the MoraBanc business group, entities which are primarily active in the financial, insurance and service sectors. The applicant is considered as having been informed of this transfer of information by means of this clause. The applicant accepts that he/she may be sent information on any product or service marketed by these companies.

The data processing manager is MoraBanc. The applicant is hereby informed that the rights of access, rectification, suppression or opposition may be exercised in the terms established in current legislation.

You may also like