Market outlook – March 2024

22 March de 2024

February closed with clear positive results in the main markets, particularly in the US market. The Nasdaq technology index showed the biggest gains, up 6.12%, while the S&P 500 was slightly lower despite rising more than 5%. The European stock markets also rose strongly and the Eurostoxx rose by almost 5% thanks to Italy’s positive performance. In Asia, February saw another strong performance by the Japanese stock market. The Nikkei rose by almost 8% and is now up more than 16% for the year.

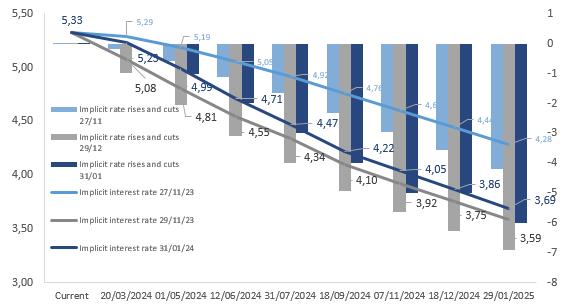

In macroeconomic terms, February brought the slowdown in inflation to the fore. The US CPI, despite surprising the market, moderated to 3.1% from 3.4% year-on-year. European figures for Germany, Spain and France were released at the end of the month as a prelude to the Eurozone aggregate data to be published at the beginning of March. All the inflation figures confirmed this slowdown, to a greater or lesser extent, with Germany’s figure standing out at 2.5%, which helped the Eurozone’s figure to 2.6%, thus getting closer to the European Central Bank’s target of 2%. These data, together with the US growth data, show strength, as evidenced by the release of the first revision of 4Q23 GDP at 3.2%, supported by consumption figures. In this context, the likelihood of interest rate cuts by central banks has been decreasing. The US has increased the probability that the first rate cut could occur in June, with a 75% probability, and the likelihood that it will occur at the April meeting has less and less support, with only a 24% probability.

Implicit market interest rate for the United States

Source: Bloomberg and prepared by MoraBanc

Forecasts by geographic areas

United States

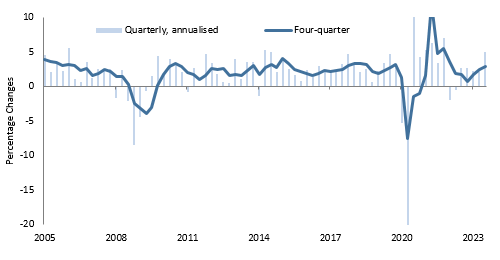

The chances for the US of a soft landing have increased, with a strong labour market, the process towards disinflation and the Fed open to cut rates this 2024.

On the other hand, demand is expected to slow down due to the depletion of savings and the impact of high interest rates, which will lead to more moderate and lower growth than last year.

USA GDP

Source: Goldman Sachs Asset Management

Europe

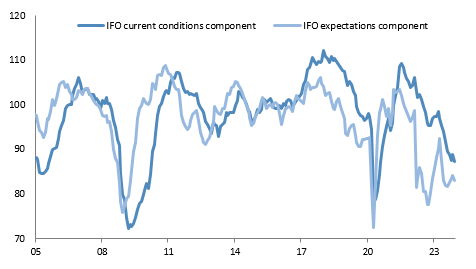

Both the IFO business confidence and PMI surveys of manufacturing and service sector confidence suggest that growth should remain close to zero, and even at risk of deteriorating. The labour market remains the key to growth prospects for the Eurozone, and the risk lies in a further rise in the unemployment rate. Moreover, the negative pressure from high interest rates should gradually moderate.

IFO Eurozone business confidence survey

Source: Goldman Sachs Asset Management