Market outlook – January 2024

16 January de 2024

December was a month of consolidation in the main variable income markets, following the exceptional rises in November, thus ending a year of strong rises. The key dates in the month were undoubtedly the meetings of the main central banks, which did not disappoint analysts, putting an end to their rate hike policies that began last year. The European markets thus closed with a double-digit increase. In particular, Eurostoxx 50 rose by almost 20% in 2023, highlighting the good performance of peripheral economies such as Spain and Italy. The Transalpine stock market stood out with a rise of almost 30%. The same trend was seen from Wall Street. The index that benefited most was Nasdaq (a tech index), which rose by more than 50% in 2023, while the S&P 500 saw an almost 25% increase.

Central banks

Central banks almost ended their monetary policy of rate hikes. The Fed ended 2023 with a rate range of 5.25-5.5%. What surprised analysts the most was the forecast for next year’s rates: three rate cuts of 25bp each have been discounted for 2024. At the press conference held by Fed chair Jerome Powell, he was optimistic about future inflation without this having to imply a significant increase in unemployment. The European Central Bank kept rates at 4.50%, 4.75% and 4.00% for the main financing operations, the marginal credit facility and the deposit facility, respectively. On this occasion there was no open talk of a start date for rate cuts in 2024.

The central banks’ decisions had a direct impact on yields in the fixed income market, so they were closely observed in government bonds. Overall, 2023 was a very positive year for the fixed income market, thanks to the rise in prices during the year’s final straight. The fall in inflation and improved expectations for next year allowed sovereign bond prices to rise sharply, putting 10-year American Treasury bonds at around 3.90% and 10-year German bonds at around 2%.

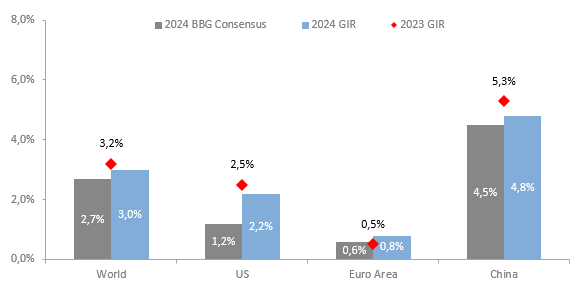

Global growth forecasts

Source: Goldman Sachs Asset Management

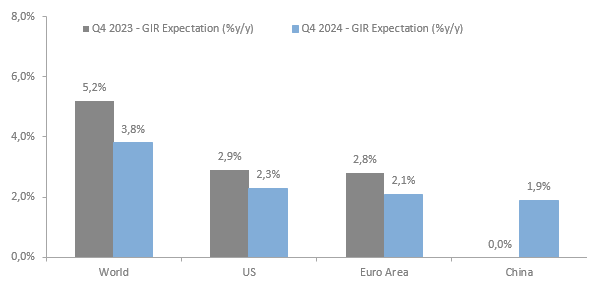

Inflation forecasts for 2024

Source: Goldman Sachs Asset Management

Ten key issues for 2024

- United States Growth: The risk of recession is receding. There will be an increasing slowdown in growth with an above-average recession risk (70% based on the NY Fed model).

- Growth divergence: Between the United States on the one hand, and Europe and China on the other. However, they may converge in the coming quarters.

- Inflation in developed markets: The process of decreasing inflation will continue, but with the occasional increase along the way.

- The Fed and the ECB: The rate hike process has been completed by the two central banks. Rates will remain at these levels throughout 2024 for longer than the market is discounting.

- Debt: Attractive returns in both the United States and Europe.

- Credit: Attractive returns in both the US and Europe with default rates around average.

- Equities: Investment opportunities outside the Magnificent Seven. Value in active management.

- Forex: Possible depreciation of the dollar.

- Asset allocation: Improved attractiveness of fixed income. It could be a good idea to hedge against market volatility.

- Risks: Global recession, restrictive financial conditions and escalation of geopolitical conflicts