Market outlook – April 2024

16 April de 2024

In the month of March the main indices closed positive, consolidating the profits at the turn of the year and highlighting the good performance of Europe: the Euro Stoxx rose almost 4%. On Wall Street the main indexes also rose, although they remained below European returns. The S&P 500 rose around 3% and the Nasdaq 2%. Once again, the evolution of the markets has been marked by central bank interventions, inflation data and geopolitical conflicts. During this month there were two surprises regarding the central banks. The first was the rate hike by the Central Bank of Japan (BoJ), regaining positive ground for the first time in 17 years. And the other was the Central Bank of Switzerland which was surprising as it was the first of the big central banks to cut interest rates by 25 basis points as well as lowering its main policy rate to 1.5%,saying national inflation is likely to stay below 2% for the foreseeable future.

Macroeconomics and monetary policy

The growth in the United States will moderate, but remain healthy. The risk of recession is remote (20-35%) with a soft landing being more likely. Europe will continue to see weak growth even though it’s about to bottom out. The disinflation process will continue, but with some short-term volatility. The key this year will be the flexibility of monetary policy.

United States: Growth in the fourth quarter of 2023 stood at 3.2% year-on-year, but at the same time the growth of the sum of labour supply and productivity growth was around 4.5% year-on-year. This explains why the labour market continued to rebalance and is now roughly where it was in 2018-19.

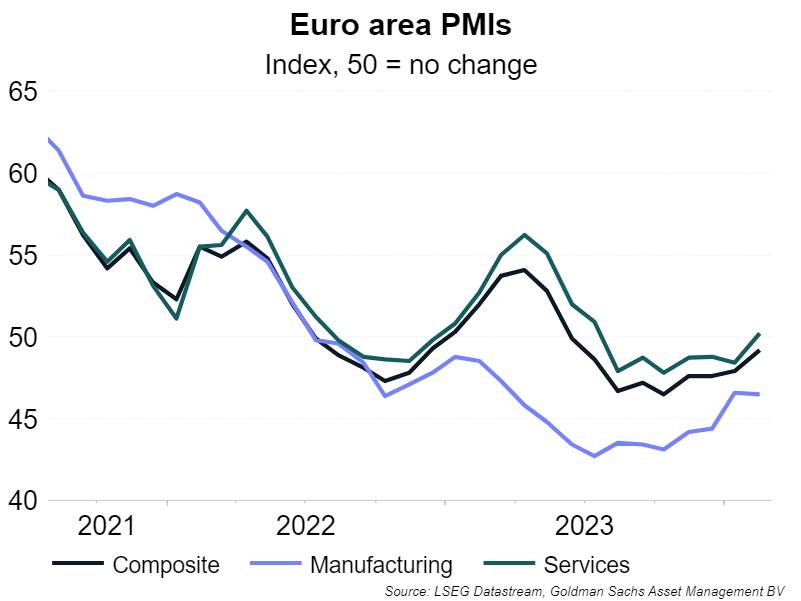

Europe: Signs of improvement (green shoots) are being seen in Europe since the turn of the year, although they are fragile. The PMI has improved, but economic sentiment is still down slightly. However, credit flow is improving slightly, and the real wage growth it is still above the long-term trend against a strong labour market. All this suggests a gradual improvement in growth.

Eurozone PMIs

Source: Goldman Sachs Asset Management

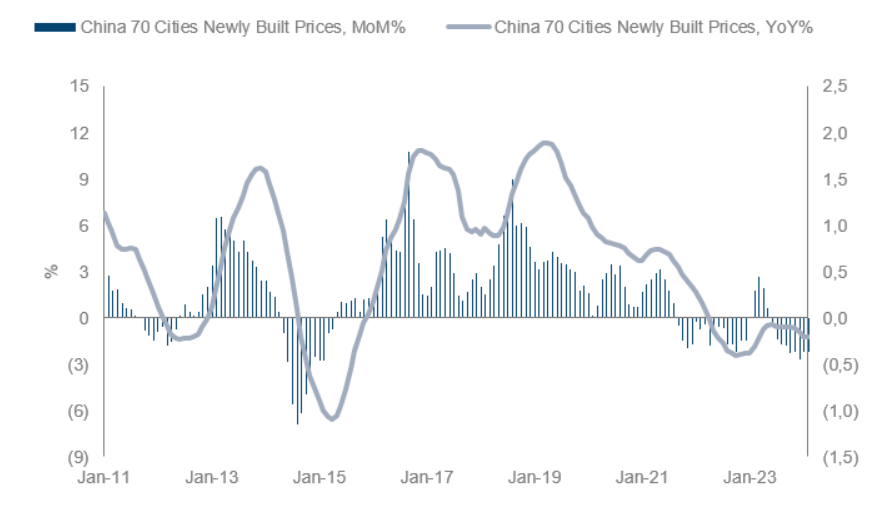

China: Given that the most relevant sectors such as real estate and exporting are in difficulties, overall growth momentum remains weak. Chinese investors remain risk averse and stimulus policies are of little relevance. The main medium-term growth risk continues to come from low business confidence due to state interventionism and regulatory uncertainty.

Housing prices in China continue to fall

Source: Goldman Sachs Asset Management

Japan: Growth is expected to be above potential this year driven by a strong labour market, improved business sentiment and accommodative monetary policy. The economy is supported by a positive feedback loop between rising inflation and nominal growth expectations, on the one hand, and falling real yields, on the other.

Market perspectives

As for the variable income market, the disinflation scenario, the expectation of a cut in interest rates, the possibility of a soft-landing scenario and earnings acceleration per share growth constitute a favourable scenario. Profit growth is expected to bounce back further this year. Valuations are high, but mostly focused on large tech companies. Basically, investor sentiment is bullish. The positioning in equity is neutral. By area, we highlight the positive global equity. This month we lower the positive on Japanese equity to neutral opting for the collection of benefits in the face of the change in the direction of Japan’s monetary policy. Preference for small companies due to being undervalued.

With respect to fixed income asset, we remain positive as rates are expected to fall in the medium term. Even so, there is a risk that inflation will be higher in the short term, which could cause lead to interest rate volatility.

As for credit, in the United States, the resilience of the US economy, disinflation and upcoming rate cuts represent support for the asset. Even so, there is a risk of a slower rate cut by the Fed and the cost of refinancing will increase as issues issued at low rates mature. The tightening of lending standards by banks and the expected slowdown in growth make us more cautious with regard to lower quality credit, and we are underweight in both American and European High Yield (at historically very low valuations). Regarding Investment Grade (IG) credit, we remain neutral even though historically credit spreads have been tight. Eurozone macroeconomic data indicate that the economy may have bottomed out. The carry remains attractive to the IG.