A volatile start to the quater

14 April de 2022

A volatile start to the quater

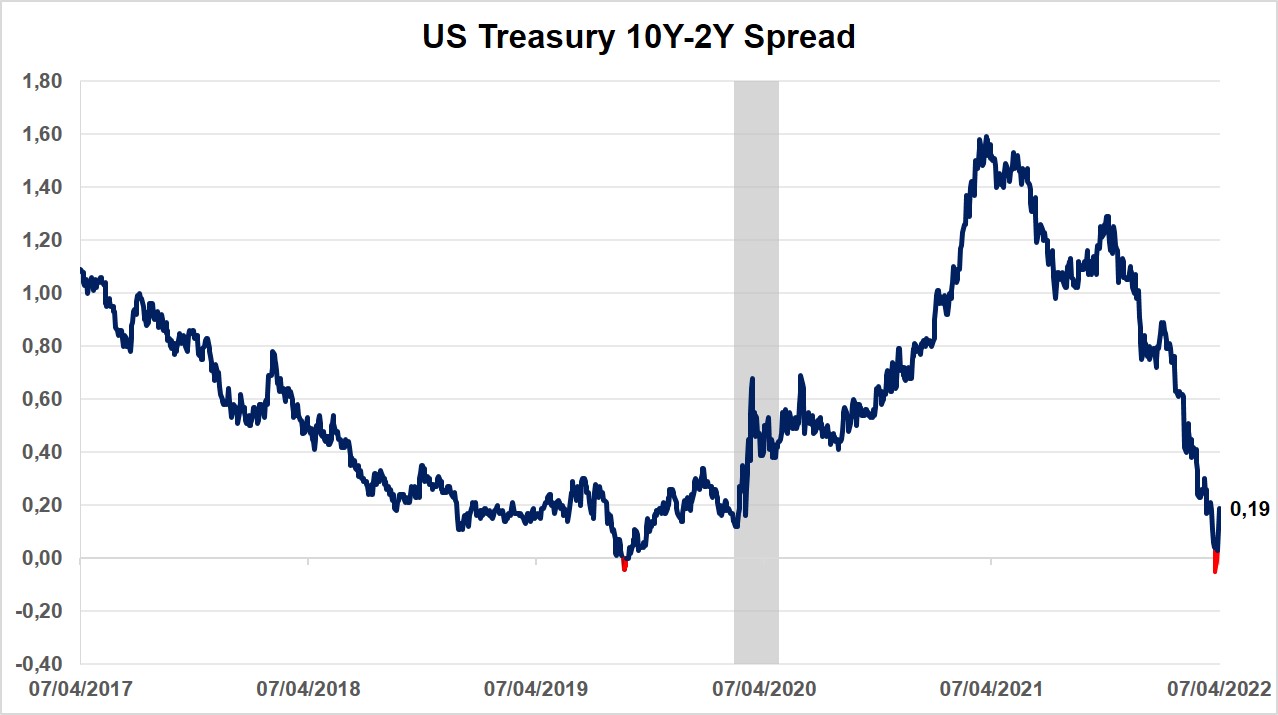

As we approach the final stretch of the first quarter of 2022, equity markets have been decidedly bullish, largely recovering from the volatility generated by the conflict in Ukraine, fears of stagflation and more hawkish central bank rhetoric. With regard to the debt market, the rise in sovereign debt yields in just a few days is particularly noteworthy, with one of the most remarkable points being the close convergence between the 2 and 10-year maturities of the US curve.

1. Raw materials

Slight declines in raw material prices, particularly oil, due to the release of reserves in several countries to increase the available supply of crude. Brent crude fell from $130 per barrel to eventually stabilise at $100 per barrel.

Despite short-term increases in the supply of some raw materials, the current shortfall resulting from of a lack of investment over the last ten years and from the surge in policies against the exploitation of some raw materials on environmental grounds, continues to put upward pressure on the prices of natural resources, keeping them at high levels.

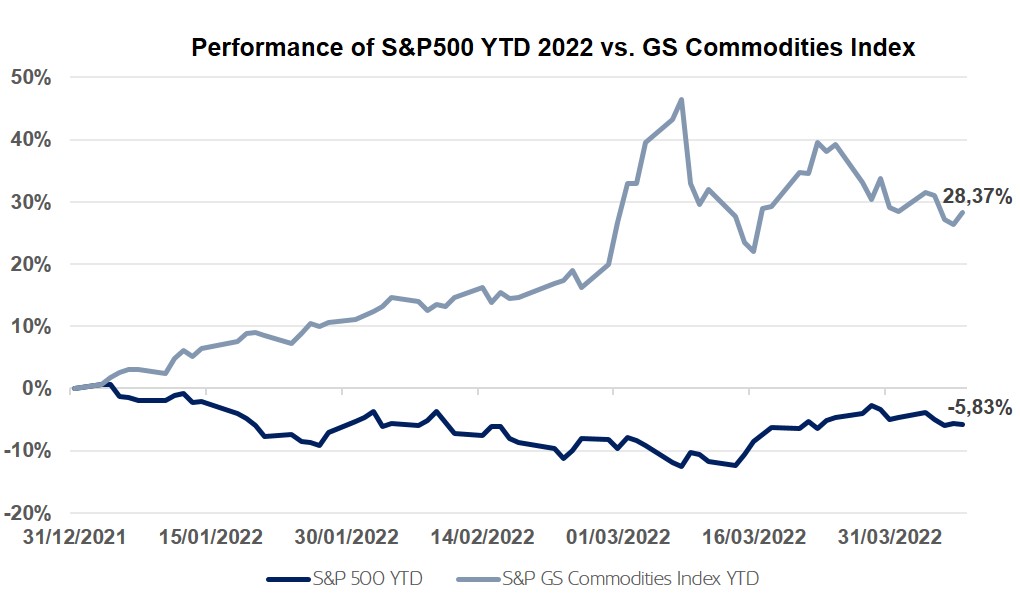

In terms of investment, raw materials are showing the best annual returns. The leading commodities index, the S&P Goldman Sachs Commodities Index, has risen more than 26% since the beginning of 2022, a difference of more than 30% over the S&P 500, one of the principal US indices, which has fallen by nearly 6% since the start of the year.

2. Central Banks maintain their restrictive tone

Central Banks have continued to be hawkish, even supporting interest rate rises to address inflation. The US Federal Reserve announced that a 50 bp hike at their May meeting was almost a reality. It also floated the possible start of a monthly balance sheet reduction of at least $95 billion starting in the summer.

In Europe, the ECB is not expected to make any change to interest rates until the autumn. The market expects a 50 bp increase this year and three or four further increases during 2023.

However, the US yield curve for 2-year and 10-year maturities was inverted for a couple of days, causing some tension in equity markets over fears that the inversion was a warning of recession.

3. Update on Ukraine

Peace negotiations between Ukraine and Russia have stalled as the tactics and strategy of Russian forces change, with a retreat towards the Donbass region in the east of Ukraine.

The United States and Europe continue to provide economic and military support in the form of arms to Ukraine, which is resisting the Russian army’s offensive. Western economic sanctions are being toughened. Europe has announced a new round of measures banning the entry of Russian ships into European ports and a ban on the import of Russian coal from August.

4. How we are positioning our portfolios

In environments like today’s, where markets are consumed by uncertainty, portfolio asset diversification has a key role. That’s why MoraBanc’s current recommendation is to stay invested, but with diversified exposure to Fixed Income and Equity.

In terms of Fixed Income, the general rise in the interest rate curve has improved fixed income’s relative attractiveness compared to just a couple of months ago, and the expected return (IRR) is continuing to rise. It is also worth remembering that Fixed Income has shown itself to be a good asset class to de-link portfolio returns in difficult times for risk assets, which is why we recommend retaining exposure to hedge possible worsening of the macroeconomic situation.

In terms of Equity, we remain positive on this asset class because the growth of the economy in real terms is expected to exceed 4% this year, well above the historic average. Also, the high valuations at which we said goodbye to 2021 have moderated, particularly in growth companies. In terms of sectors, we are positive in cyclical industries such as energy and finance.

#MoraBancExperts