Market feeling remains subdued but fundamentals remain robust

16 May de 2022

Market feeling remains subdued but fundamentals remain robust

The first weeks of May again bring a rise in volatility and new lows for the year in both equities and fixed income. These falls are despite a less harsh speech than expected by the chairman of the Federal Reserve and despite first quarter business results that are again positively surprising. Geopolitical tensions, as well as uncertainty in China, continue to dominate market movements, although most economic data continues to point to healthy economic growth overall.

1. Fed’s speech and economic data are not enough to calm the market

At the last Fed meeting, rates were raised by 50 bp to 0.75% -1% and, on a positive note, 75 bp increases were ruled out at subsequent meetings. This aspect, together with the announcement of the start of the balance sheet reduction from next June, led to the US Treasury curve returning to a certain slope.

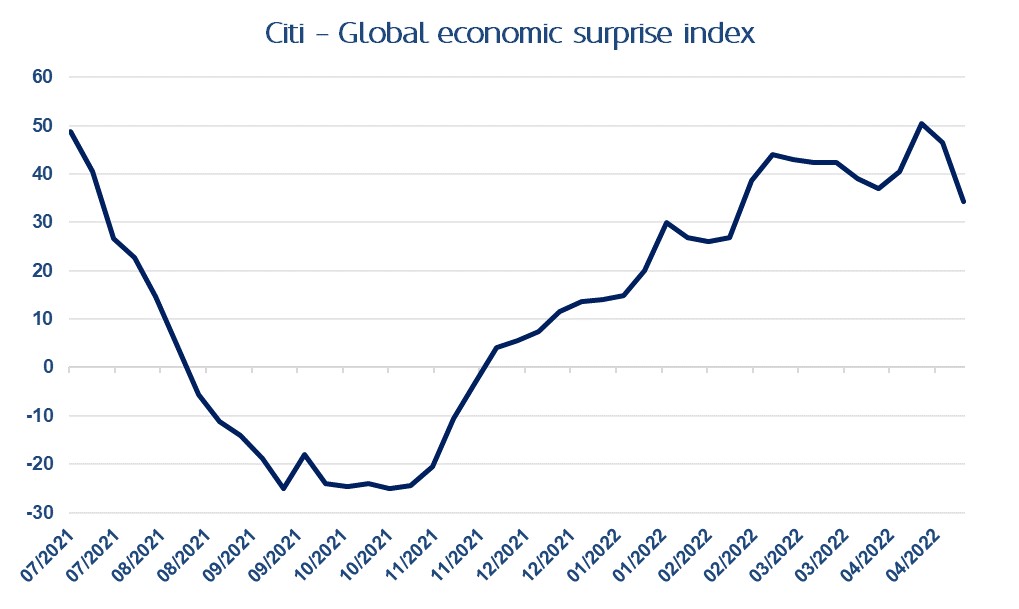

One aspect that denotes the current gloomy market sentiment is shown in the economic surprise data. The main indicators remain at clearly positive levels, indicating that economic data is proving to be considerably better than analysts predict. As we pointed out, this situation is not so much because the data is particularly strong (but robust), but because analysts are infected by the current pessimism of the market.

Bloomberg. 16/05/2022

Bloomberg. 16/05/2022

2. Good business results coupled with falls are significantly lowering equities

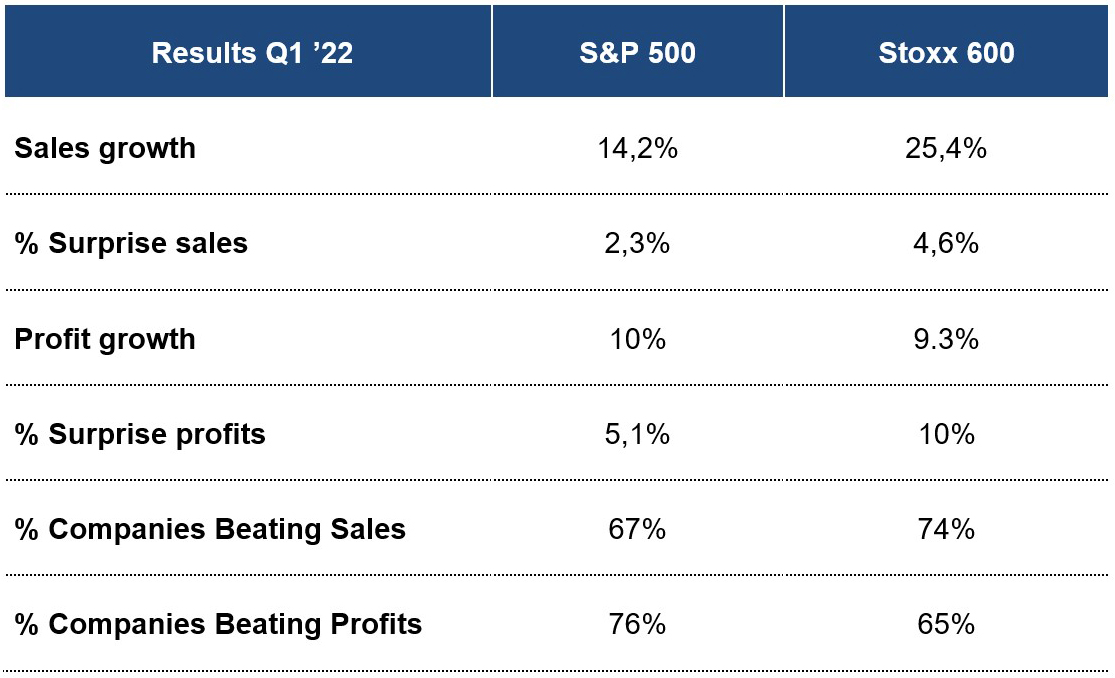

This lack of confidence is reflected in equity prices with cumulative falls of more than 15% despite analysts’ expectations that global corporate profits will grow by around 10% this year. This is in line with the first quarter of the year which, the vast majority of global companies having already reported, shows income growth of more than 14% (favoured by inflation) and, more importantly, profit growth of around 10% (both compared with the first quarter of 2021).

These results, which give some validity to analysts’ expectations for 2022, coupled with the notable falls in the current year, mean that markets have chaepened by more than 20% -25% in a matter of months. It can be argued that certain sectors started with demanding valuations at the beginning of the year. It is hard for us to see, however, that today, in aggregate terms, equities are expensive. Important regions such as Europe, Emerging and Japan are trading below their historical average and by no means above 14x the expected profits of 2022. Yes, it is true that the US is still slightly above this average, at about 17x profits, but it is undeniable that the high quality and growth of a very important part of the companies that make up its indexes makes them worthy of this premium of 10-15% with respect to historical values.

Bloomberg. 16/05/2022

Bloomberg. 16/05/2022

As is usual in our field, when market pessimism is so severe, it is automatically reflected in asset prices. We are all part of the market and therefore in a short period of time the market is sovereign. In short periods, the market tends to move like a pendulum, often deviating significantly from the real value of different assets. In the long run, however, market prices tend to be efficient and follow the evolution of business profits (in the case of the value of companies).

It is true that there are still certain assets that we continue to avoid or underweigh, such as high durations and government bonds in fixed income or the fashion sectors and companies with very high multiples in equity. But we are beginning to find many assets in which the pendulum has swung away from putting on the brakes, and offers profitability in the future. These days, we find opportunities in assets as diverse as certain segments of corporate debt or quality companies in sectors as diverse as technology or industry.

#MoraBancExperts