Political uncertainty in the United States and Europe was a key feature of October, particularly the partial shutdown of the US government and the budget crisis in France. Trade tensions between the US and China initially escalated but then eased, and monetary policy expectations were adjusted. The Federal Reserve cut its key interest rate by 25 basis points to a range of 3.75%–4.00%, although Chairman Powell dampened expectations of a further cut in December. However, the US labour market continues to show signs of moderation and inflation remains high. In Europe, the ECB kept interest rates unchanged, while activity indicators showed strength with a higher-than-expected GDP reading and subdued CPI close to 2%. In Asia, the Bank of Japan kept interest rates unchanged, while a change in leadership saw Sanae Takaichi become the new prime minister, whose agenda focuses on proactive fiscal policy and investment in technology and defence.

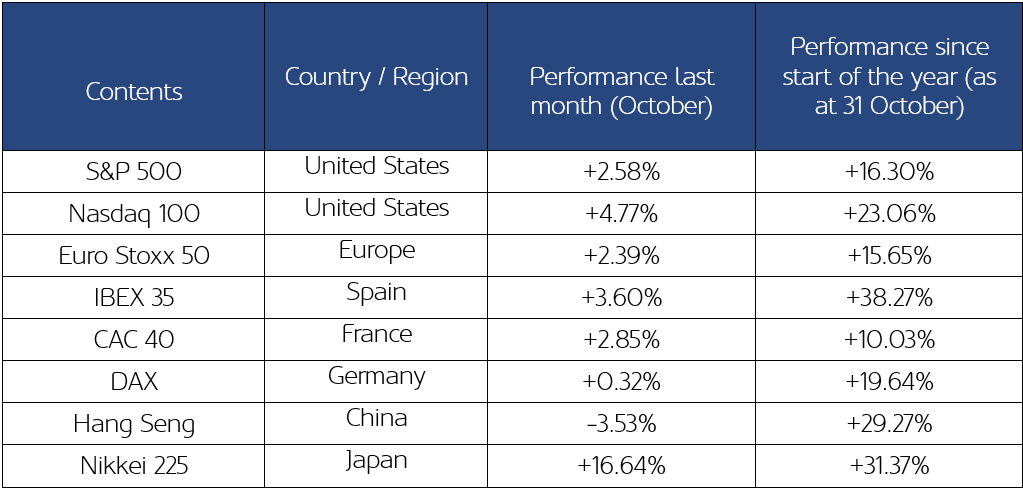

Performance of the main global indices

Source: Bloomberg and prepared by MoraBanc

Expectations of easing monetary policy did not prevent global stock markets from closing October on a positive note, ignoring multiple sources of uncertainty. The S&P 500 reached new all-time highs on Wall Street, driven by strong results from big tech companies and a trade agreement between Trump and Xi Jinping. In October, the Nasdaq 100 led the way with a 4.77% rise, while the S&P 500 and the Dow Jones advanced 2.27% and 2.51%, respectively. Markets in Europe also reacted positively to the third-quarter earnings season: the Euro Stoxx 50 gained 2.39%, and the Ibex 35 once again stood out as the leading index with a monthly gain of 3.60% (accumulating 38% so far this year). A partial shutdown of the US government interrupted the publication of macroeconomic data, fuelling volatility. The US administration has now been shut down for more than 30 days, leaving thousands of federal employees without pay. As the situation drags on, the final impact on GDP will be greater. Political instability intensified in France with the resignation and subsequent reappointment of Sébastien Lecornu as Prime Minister.

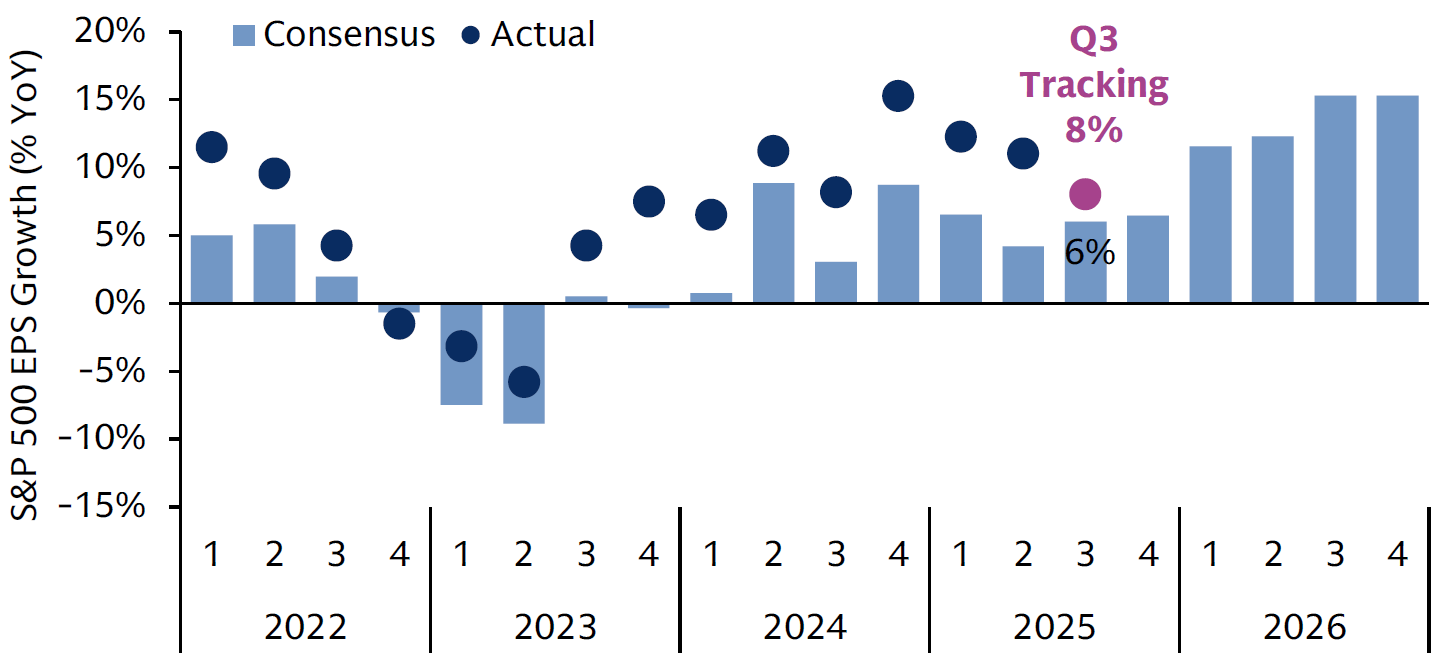

Third-quarter earnings of S&P 500 companies

Source: Goldman Sachs GIR & GSAM (29 October 2025)

As 72% of S&P 500 companies have already reported their third quarter results, earnings per share (EPS) are up 8% year-on-year, exceeding the 6% consensus forecast. This trend of better-than-expected results has continued over the last twelve quarters.

Volatility in fixed income markets caused significant narrowing in the Treasury yield curve. The 10-year US bond yield fell 7 basis points to 4.08%, although it did dip below the 4% threshold (October 2024 low) due to increased demand for safe-haven assets. However, at the end of the month, yields rebounded slightly following the thaw in trade relations with China and Powell's more restrictive tone. Sovereign curves also narrowed in Europe, with the 2-year Bund yield falling 5 basis points to 1.97%. As for currencies, the euro weakened in October to $1.1524, with a monthly variation of -1.98%. Commodity prices saw Brent crude oil fall to $65.06 per barrel and hit a five-month low ($61/bbl), pressured by concerns about oversupply and global growth. Gold experienced strong volatility, exceeding $4,000 per ounce and reaching historic highs of $4,348, driven by demand from central banks and trade tensions. However, a technical intraday drop of -6.3% preceded a downward trend, closing the month flat at $3,998. Finally, bitcoin fell -1.94% to $107,868 in a volatile month marked by trade tensions.