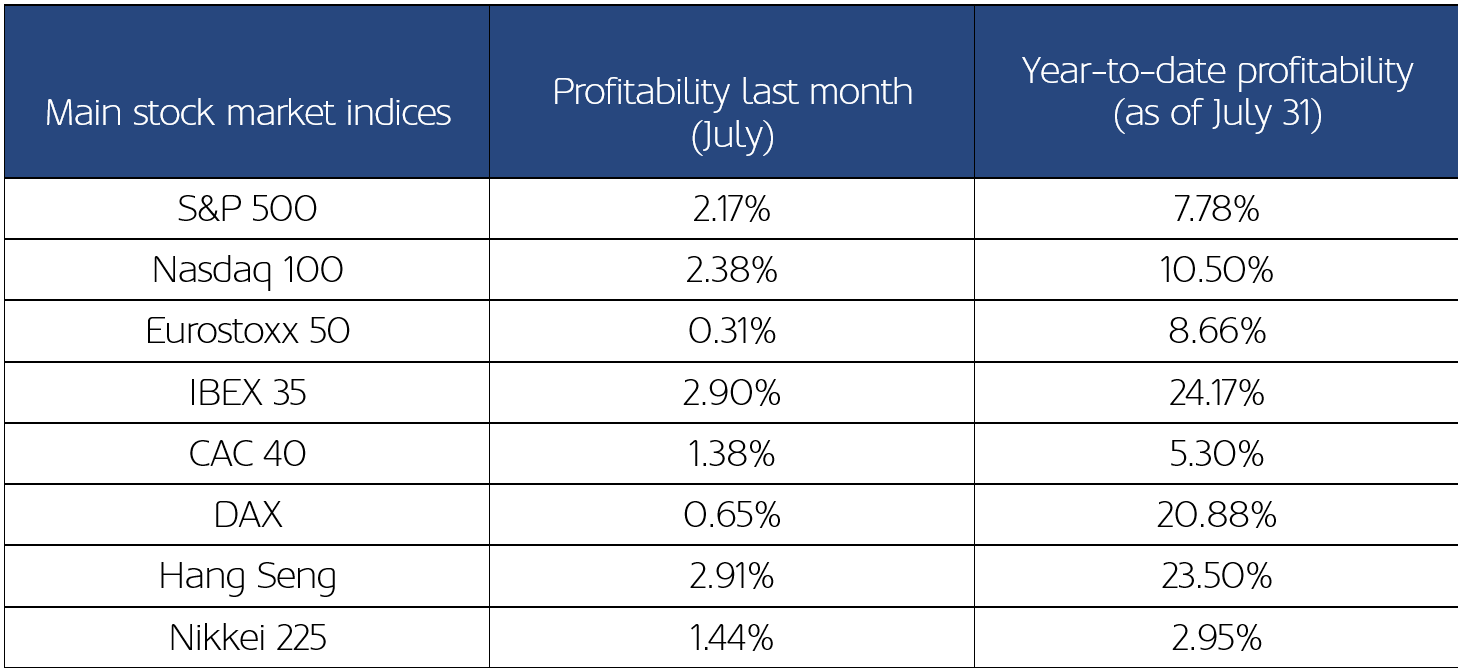

The month of July was marked by trade agreements reached between the United States and its main trading partners: Philippines, Vietnam, United Kingdom, Japan and, finally, the European Union on the 27th. In the latter case, a maximum tariff of 15% was agreed on European exports to the US, with exemptions for certain strategic products. In addition, Brussels committed to purchasing up to $600 billion in American energy and defence goods. The markets welcomed the convergence of positions with optimism, backed up by a season of better-than-expected second-quarter corporate earnings in general terms. In the United States, the S&P 500 was up 2.17%, marking the third consecutive month of gains. The Nasdaq 100 rose 2.38%, while the Dow Jones virtually flat-lined, with a slight increase of 0.08%. In Europe, the main indices also closed in the green: the Eurostoxx 50 appreciated by 0.31%, remaining pegged to the 5,300 point area.

Performance of the main stock market indices

Sources: Bloomberg and prepared by MoraBanc

In the macroeconomic field, data from the United States was mixed: a clear slowdown in the labour market and higher-than-expected inflation were noted, although real GDP surprised positively with respect to consensus. In the Eurozone, inflation remained steady at 2%, in line with the ECB's target.

In terms of monetary policy, the main central banks chose to keep interest rates unchanged, reflecting a cautious approach to economic and commercial uncertainty. The European Central Bank left the price of money unchanged for the second consecutive month, with Lagarde highlighting the economy’s resilience and warning of tariff-related risks. In the US, the Federal Reserve also kept the benchmark interest rate within the 4.25%-4.50% range, despite tensions between Trump and Powell. The most notable development was the internal disagreement within the FOMC: two members voted in favour of a 25 basis point cut, something that had not occurred since 1993. This disagreement increased hopes of a downward adjustment in September, although the decision will depend on the outcome of the data.

In such a context, fixed income markets experienced high volatility. In the US, the 2-year Treasury yield rose more than 20 basis points, to 3.957%, amid increased odds of an accommodative turn. In Europe, sovereign yields also rose: the 2-year German Bund climbed to 1.96% and the equivalent Spanish bond to 2.08%.

In the foreign exchange market, the euro depreciated by 2.89% against the dollar, closing at $1.14, dragged down by the improved tone on trade coming from the United States. In raw materials, oil stood out with a sharp monthly rise: Brent futures rose 7.28% to $72.53 per barrel, driven by sanctions on Russian crude and stronger-than-expected seasonal demand. On the other hand, gold remained stable in a context of contained volatility, ending the month at $3,295 per ounce, very close to where it was in early July.

EUR/USD evolution YTD

Sources: European Central Bank