August was characterised by the declarations of Federal Reserve chair Jerome Powell at the annual symposium of central bankers held in Jackson Hole, during which he opened the door to a potential cut in interest rates at the meeting in September. Powell indicated that the focus of the monetary authority is gradually shifting towards the labour market and relegating inflation to the background. The prospects of an accommodative turn in the US monetary policy boosted North American equities and had a positive impact on other international markets. The second half of the second-quarter results season also boosted investor optimism due to the overall positive balance. Despite certain intra-month adjustments motivated by doubts about the continuity of the technological rally and the signs of deterioration in the labour market, the main indices closed with gains. The S&P 500 and the Nasdaq 100 reached record highs during several sessions and underwent respective 1.91% and 0.85% rises. In Europe, the Eurostoxx 50 recorded a more moderate 0.60% increase, backed by stable macroeconomic indicators.

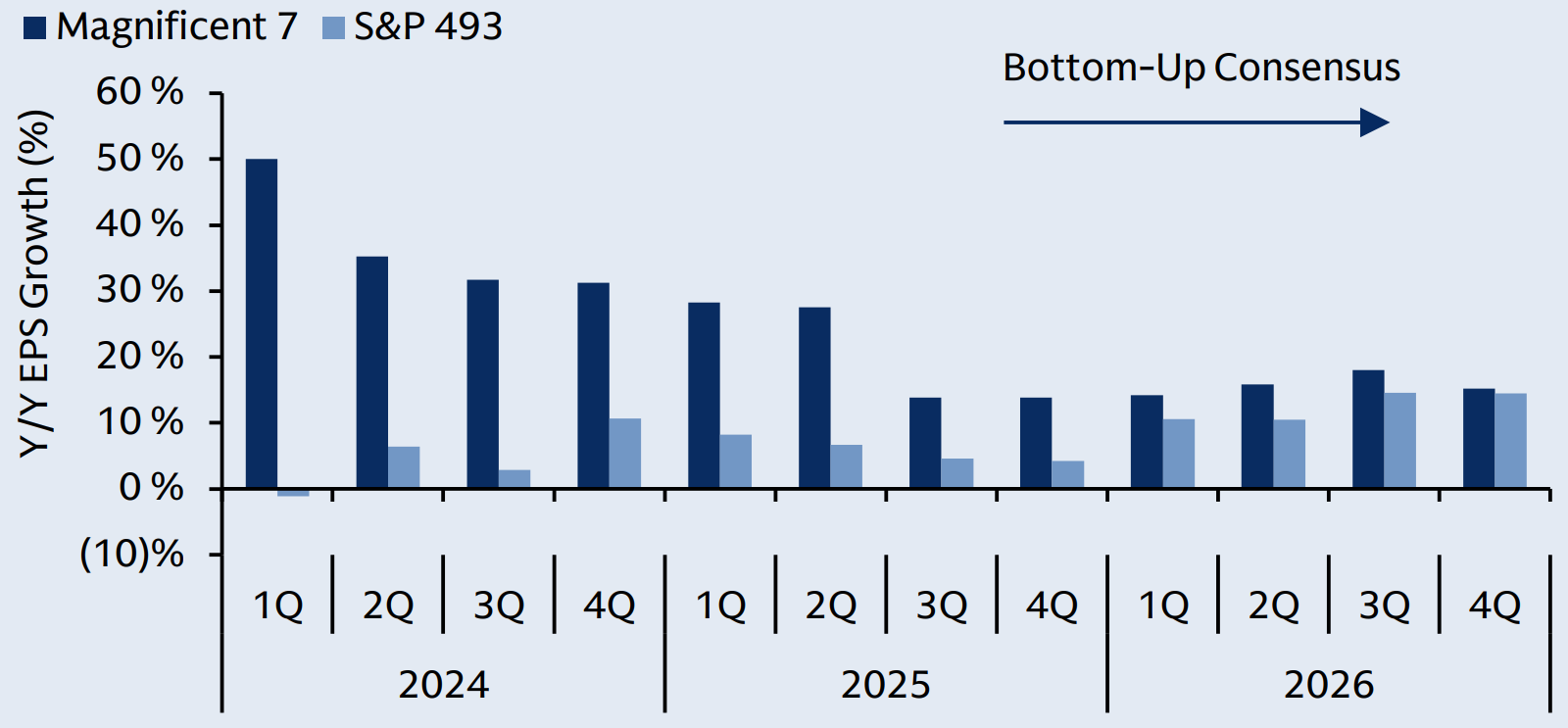

Increased profits for the “Magnificent Seven”

Sources: Goldman Sachs GIR & GSAM (28 August 2025)

The second-quarter results season reaffirmed the exceptional nature of the large-caps’ technology stock profits, challenging the market’s expectations that the gap between the earnings of the “Magnificent Seven” and those of the rest of the S&P 500 would narrow in the short term.

In the field of trade policy, a new round of tariffs came into force, affecting over 90 countries, including Switzerland (39%), Brazil (50%) and India (50%). The latter country’s rate was increased by 25 percentage points by way of a penalty for its imports of Russian crude oil. However, at the end of the month, the US federal court of appeals declared most of the tariffs decreed by President Trump illegal, although they will remain in force until 14 October to allow for a potential appeal by the White House.

In the macroeconomic sphere, the US labour market showed signs of cooling, with an increase in applications for unemployment benefits and renewals. However, second-quarter growth was revised upwards to 3% year-on-year, reversing the -0.5% slowdown recorded in the first quarter. Headline inflation (CPI) remained at 2.7% year-on-year, slightly below the forecasts, while the core PCE recovered to 2.9% and the monthly PPI rose by a considerable 0.9%. In Europe, inflation remained stable at 2%, with ECB president Christine Lagarde ruling out any further rate cuts until the trade scenario is clarified. Growth in the eurozone was revised slightly downwards to 1.4% year-on-year, while the manufacturing PMI returned to expansionary territory and reached its highest level in over three years. In the United Kingdom, the Bank of England cut its rates by 25 basis points to 4%, although inflation rose to 3.8% year-on-year. The indicators were weak in China, with an upturn in the unemployment rate and a slowdown in the growth of industrial production and retail sales.

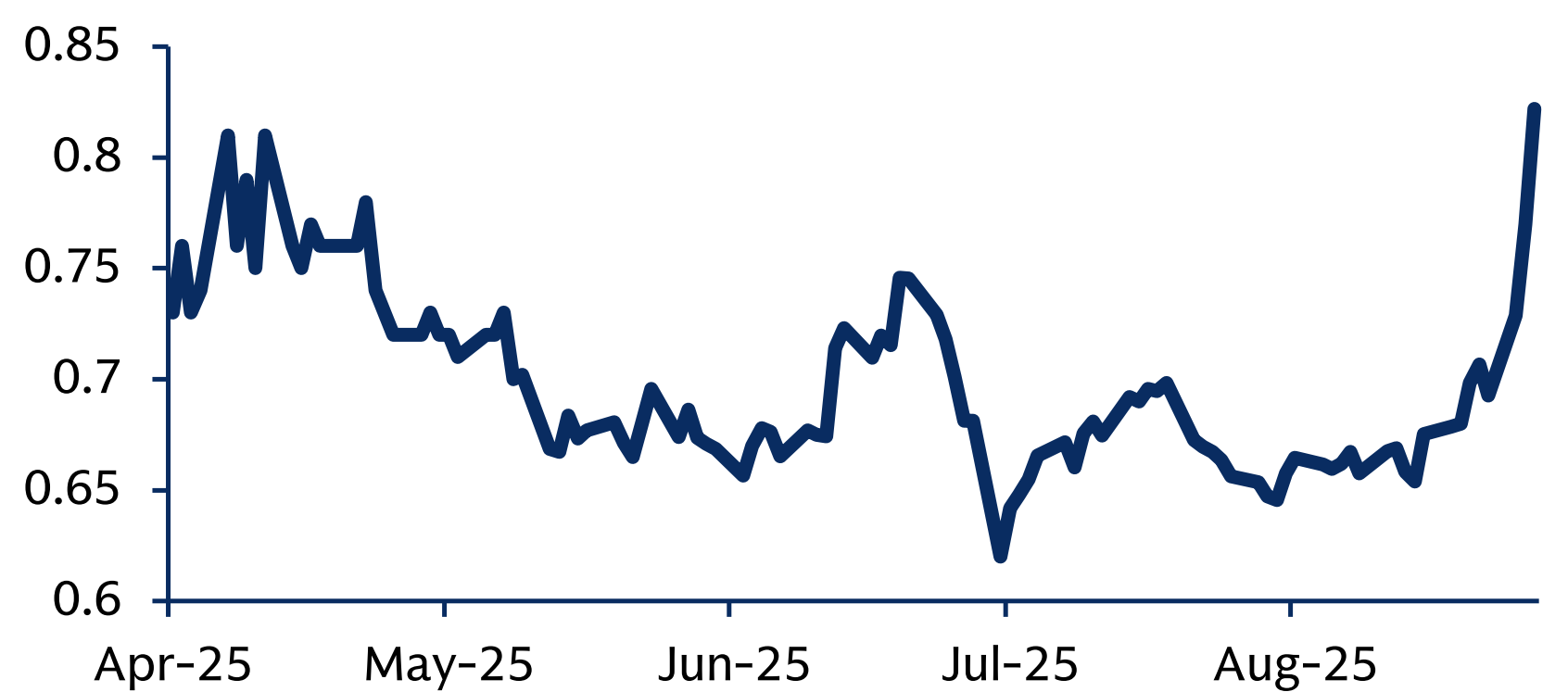

In the fixed income markets, the yield on the 2-year US sovereign bond fell by almost 35 basis points to 3.61%, weighed down by Powell’s declarations and the increasing likelihood of a downward adjustment in rates. In Europe, the yield on the 10-year German Bund rose slightly to 2.72%, coinciding with a further slowdown of the German GDP (-0.3% quarterly). The IRR of its French counterpart climbed by 16 basis points to 3.51%, within a context of internal political tension, as Prime Minister François Bayrou will face a no-confidence vote on 8 September following the failure of his budget plan, which envisaged significant cuts in public spending.

French and German 10-year bond spread

Sources: GSAM (27 August 2025)

With regard to currencies, the euro appreciated by 2.37% to $1.1686, pushed upwards by doubts about the independence of the Fed and expectations of cuts. As for raw materials, crude oil underwent significant volatility and closed with a fall of 6.08% to $68.12 per barrel, beset by the sanctions on Russian oil and geopolitical tensions. Gold continued its upward course, rising by 4.80% during the month (+31.38% since the start of the year) and reaching a new high of $3,448 per ounce, driven by the search for safe haven assets in view of the instability. Finally, Bitcoin reached an all-time high of $122,952 in the middle of the month, but fell back to $109,127 in the latter part of August.