2025 has been a year characterised by optimism among investors. Despite geopolitical risks within the context of a transitional monetary policy, the main asset classes have maintained their positive behaviour, with all-time highs in terms of equity, high flows towards risk assets and healthy demand for alternative assets such as gold.

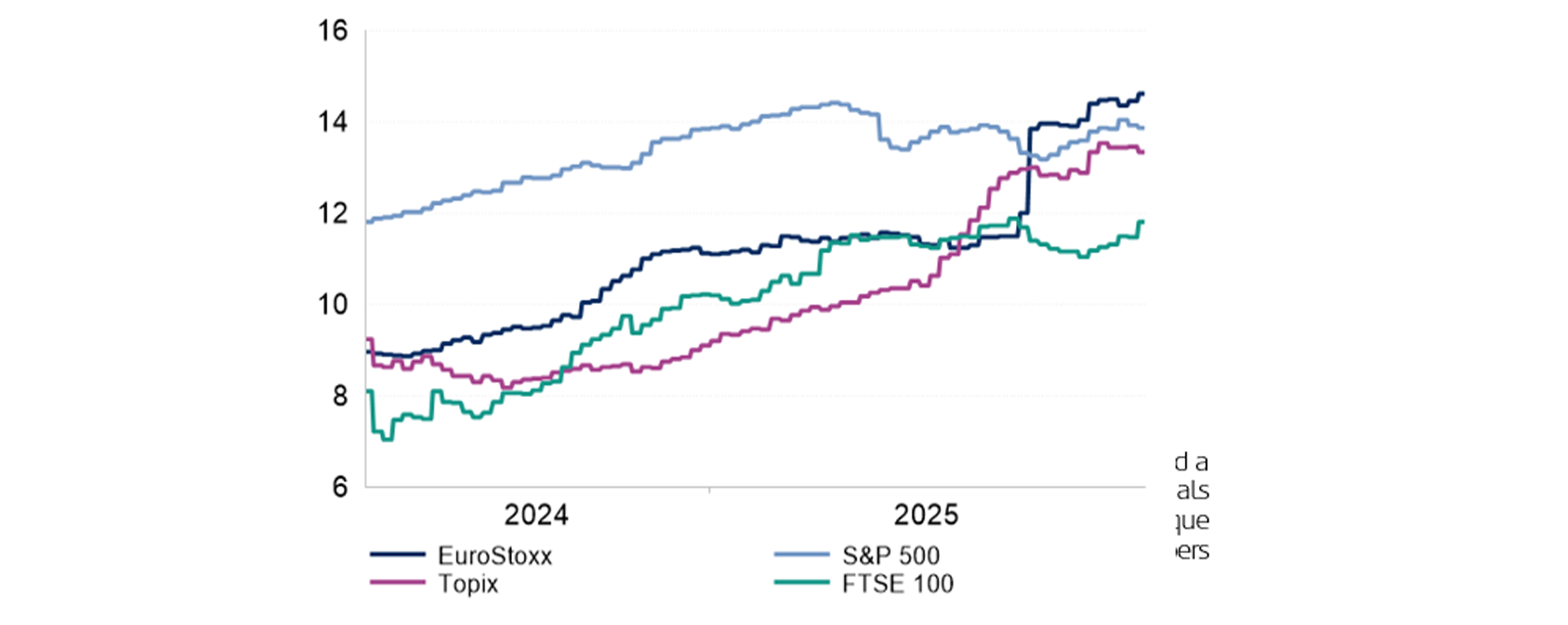

The stock markets remain at very high levels, reflecting investor confidence within a scenario of stable growth and controlled inflation.

Despite the above optimism, cross-sectional volatility is still a distinctive feature of the current markets. In the United States, the concern is based on the high valuations and the sustainability of public debt, while in Europe attention is focused on the expansionary fiscal policy and its potential to reactivate growth.