Presentation of quarterly results

19 October de 2022

The Federal Reserve has raised its key rate by 3 percentage points since March, the fastest pace of increases since the early 1980s.

The minutes of the Fed’s September meeting, released on Wednesday 12 October, showed that many of its members have yet to see any progress in their fight against inflation.

The recessionary pressure is becoming more and more intense, and the idea of a soft landing by slowing the growth of the economy enough to control inflation without pushing the economy into recession is looking more and more like a utopia.

The world economy, weakened by rising energy prices as a result of Russia’s war against Ukraine, is at a turning point.

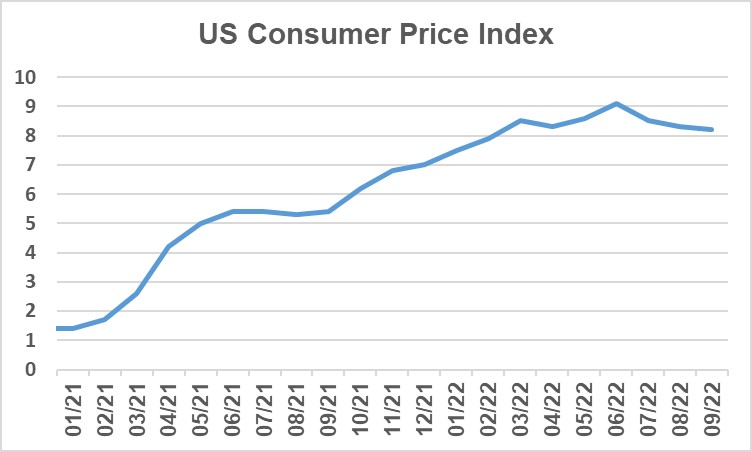

1. US Consumer Price Index.

The Consumer Price Index (CPI) rose by 0.4% in September in the United States, bringing annual inflation to 8.2%. These figures show a slower than expected deceleration.

The rise was mainly explained by the strength of the services sector, reflecting a re-acceleration of inflation in rents, food and medical expenses, which are at August highs.

On the other hand, it is worth noting that petrol prices fell in September, which has helped to partially contain the overall CPI.

The core Consumer Price Index, which excludes food and energy, increased by 6.6% over the previous year, the highest level since 1982. Since the previous month, the core CPI rose by 0.6% for the second month.

It should be noted that this is the last official CPI data before the midterm elections scheduled for 8 November.

On the other hand, on Friday 7 October, the US labour market data were good and consistent.

Persistently high inflation and labour market rigidity allow the US central bank to maintain its aggressive monetary policy for longer.

Graph 1: US Consumer Price Index

Source: Bloomberg

Data comprising the period from 01/01/2021 to 01/09/2022

2. Third-quater corporate earnings reports kick off

The third quarter earnings season begins on Wall Street, a very important test for the market as investors are braced for what could be one of the worst reporting seasons in the last 2 years.

The profit growth rate of the S&P 500 is expected to be only 2.9%, which, if confirmed, would be the lowest year-on-year growth since the third quarter of 2020, at the height of the pandemic.

The energy sector is the one expected to stand out on the positive side of the table. The sector’s income is expected to increase by 35.6% year-on-year due to higher oil and natural gas prices. Let us recall that the average price of WTI crude oil in the third quarter of 2022 was 91.62 dollars per barrel, 30% higher than a year ago.

In contrast, the telecommunications sector in particular, within the communications sector, is expected to experience a 13.2% drop in income year-on-year.

#MoraBancExperts