Market perspectives

8 May de 2023

In April, after the stock markets were shaken by the high volatility due to the financial crisis that originated in the United States, and their subsequent recovery, the indices continue to be positive: the Euro Stoxx 50 has risen during the month of April by 1.027% (from 31/03/2023 to 28/04/2023) and the S&P 500 up to 1.46% (from 31/03/2023 to 28/04/2023).

Macroeconomics and monetary policy

Weak growth is expected in the United States as a result of a still restrictive monetary policy, but also due to the impact of the banking crisis, which will affect the granting of credit and therefore will end up impacting growth.

In the eurozone, growth is also expected to be weaker and, in this respect, both economies are expected to grow below the trend this 2023, with a high risk of mild recession. Global growth should benefit from improved growth in China (forecast of 5.5%-6% in 2023, benefiting from reopening and supportive policy).

Inflation is expected to slow down but it will still be relatively high in the short term, especially in Europe and the United Kingdom. In the United States, inflation is expected to moderate in 2023, but short-term risks of high inflation remain, given the strength of basic services and a certain upturn in the prices of second-hand cars.

Apparently, central banks will have to continue with a restrictive monetary policy, albeit combined with the necessary tools to maintain stability in the financial system. But it seems that we are now closer to the end of the tightening policy in the United States; this is what the Federal Reserve has hinted at after its meeting in May where it ended up raising rates by 25 bp and placing them in the range of 5%-5.25%, the highest since 2007 and the gateway to the end of the cycle of rate hikes.

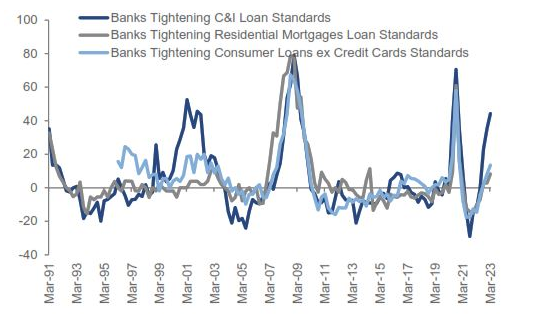

Potential impact of tightening credit standards on US GDP growth

The recent concerns surrounding the banking system are mainly due to three factors:

- The duration mismatch: Banks have investments with very long maturities that have suffered significant market losses as interest rates have been rising.

- The flight of deposits: Given lower interest on bank deposits, clients are shifting from bank deposits to monetary market investment funds, which absorb interest rate hikes faster and generate higher returns. As a result, banks may lose deposits or have to offer a higher interest rate, which may affect profitability and future lending.

- Loan losses: Uncertainties regarding commercial real estate (CRE) loans caused by higher rates, higher refinancing costs and higher sensitivity to floating rate debt have raised concerns among regional banks, given their greater exposure to CREs.

As a result of tighter monetary policy and banking sector concerns, credit standards are expected to tighten, which could reduce GDP growth by 50-100 bp this year.

If the tightening of credit standards accelerates outside CREs, the impact on growth could be more significant.

Banks tighten their lending conditions

Source: Multi Asset Solutions Goldman Sachs, Global Investment Research Goldman Sachs, Bank of America Merryll Lynch, Ivashina & Scharfstein (2010) and Haver Analytics

Equity

Downside risk has remained high with heightened macroeconomic, political and corporate profit uncertainty. The possible spread of the regional banking crisis to the wider economy, through tighter bank lending rules, may end up affecting economic growth prospects and increasing the risk of recession. So far, equities have held up relatively well, despite these headwinds. Highly leveraged sectors are the most vulnerable.

In a context of greater uncertainty, together with the expected weakness in microeconomic fundamentals, we maintain a position of caution and underweight in equity.

Fixed income

Fixed income has brought lower rates and the profitability has moderated.

Credit spreads, which widened with the financial instability caused by the bankruptcy of Silicon Valley Bank, have opened up opportunities in investment grade credit. Although the expansions have moderated during the month of April, we still think it is interesting to continue building a portfolio in high-quality corporate debt.