The first month of the year ends with widespread upturns

4 February de 2023

January closes with rises in almost all assets. Europe has excelled, with the Euro Stoxx 50 up almost 10% due to the easing of the energy crisis, temporarily forgotten as a result of the abnormally warm weather in recent weeks, which has led to low gas consumption and the resulting drop in electricity prices. Similarly, fixed income, particularly of the long-term kind, has begun to recover after a dismal 2022, driven by the inflation numbers, which continue to let up.

The inflation numbers continue to ease

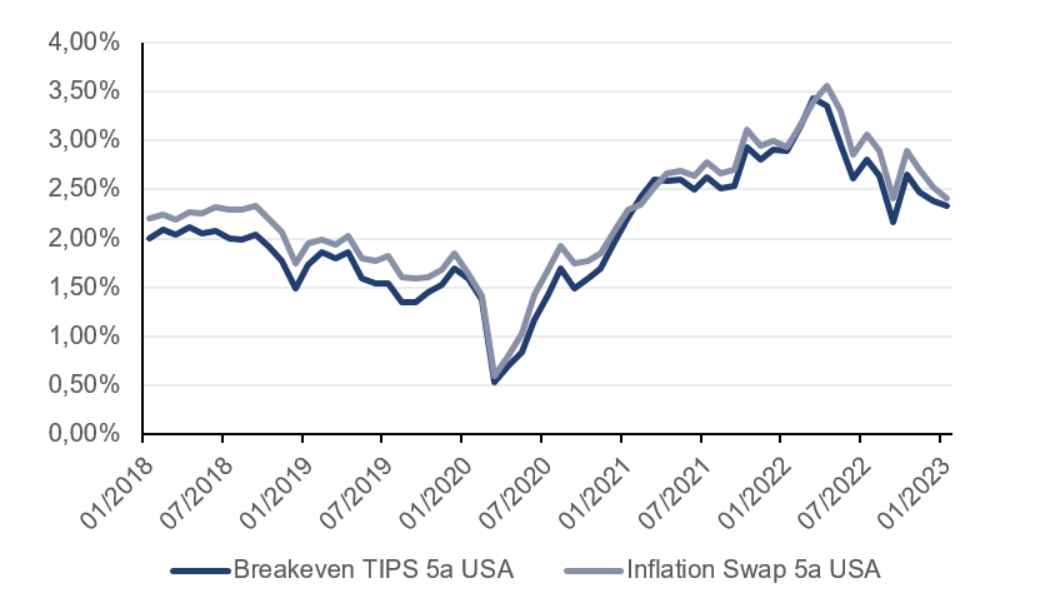

As we indicated in November: “While it’s true that it’s still very early to declare that inflation has been overcome, in the short term everything points towards the upward pressure on prices continuing to diminish.” In this respect, inflation has continued to ease, with year-on-year and month-on-month increases clearly lower than those seen in the first half of 2022. The positive direction of the inflation data has allowed the market to rule out an easing of interest rate hikes and even two rate cuts by the end of 2023 in the US. Logically, this factor has boosted financial assets, as it means lower discount rates for future cash flows (or, at the very least, the stabilisation of this rate, which kept rising in line with central banks’ decisions) and less likelihood of entering a recession (due to the lower financial pressure on companies, families and governments).

Although we still believe that inflation will remain under control in the coming months, we aren’t so sure in the medium and long term. The market is anticipating a return to inflation levels in line with those of the last decade, and at MoraBanc Portfolio Management we believe that there are clear upside risks. After all, (1) the world continues to move towards a current deficit situation in most commodity and energy markets, (2) the globalisation process is in many cases being reversed, and (3) history tells us that when inflation exceeds 5%-7%, it usually takes years for it to normalise below 3%.

5-year inflation hedge market price in the US and 5-year implicit price quotation of inflation-hedged bonds in the US

Source: Bloomberg

Meanwhile, China normalises its zero-COVID policy

Suddenly, in just two months, China has loosened its restrictive social and mobility-based policies. This normalisation is reactivating mobility in the country, and we’re likely to see an upturn in economic activity; the market consensus once again envisages growth more in line with the pre-COVID situation (an annual 5%).

After two years during which both the Chinese stock market and the emerging stock markets have undergone significant falls, the last months of 2022 and the beginning of this year have seen a considerable change in trend. Without any great degree of certainty as to the performance of the two assets in the short term, over longer time frames we believe that emerging equities should offer good returns, given the current depressed valuation levels (11x P/E forecast next 12m), in contrast to the more rigorous valuations of Western markets such as the US (17x).

After a very poor 2022 for most assets, 2023 has begun on a more favourable note. While it’s true that Portfolio Management has slightly reduced its equity investment levels, in general we remain invested. Despite the recent increases, our job is less difficult today than it was in early 2022, when the vast majority of assets were expensive from a valuation point of view. Despite the strong performance in recent months, many fixed income assets offer value and favourable medium-term return prospects. Meanwhile equity has become cheaper in the wake of the falls in 2022, which means that, when it comes to building portfolios, the prospects for returns are significantly better, with particular emphasis on the most conservative portfolios, mostly made up of fixed income assets. For example, in the portfolios managed by MoraBanc we’re over-weighting assets such as bonds linked to short-term inflation, emerging equity and small Japanese companies; these are assets that are trading at lower levels in a historical context, but we think they have good prospects in terms of their future performance.